We are in the “Winner Takes Most” Golden Era.

In my two prior newsletters — Why 2025 is the Start of a Golden Era for Startups and The 2026 Venture Outlook: The Winner-Takes-Most Golden Era — I made the case that we are entering a gold rush for startups. I also warned that this golden era was not evenly distributed. Capital was concentrating in fewer deals, fewer firms, and fewer geographies than at any point in the past decade.

The Q1 2026 data from NVCA-Pitchbook Venture Monitor is now in. The thesis holds, but the magnitude has exceeded every expectation.

Here are six takeaways from the data, and what each one means for founders navigating the AI Power Law Era.

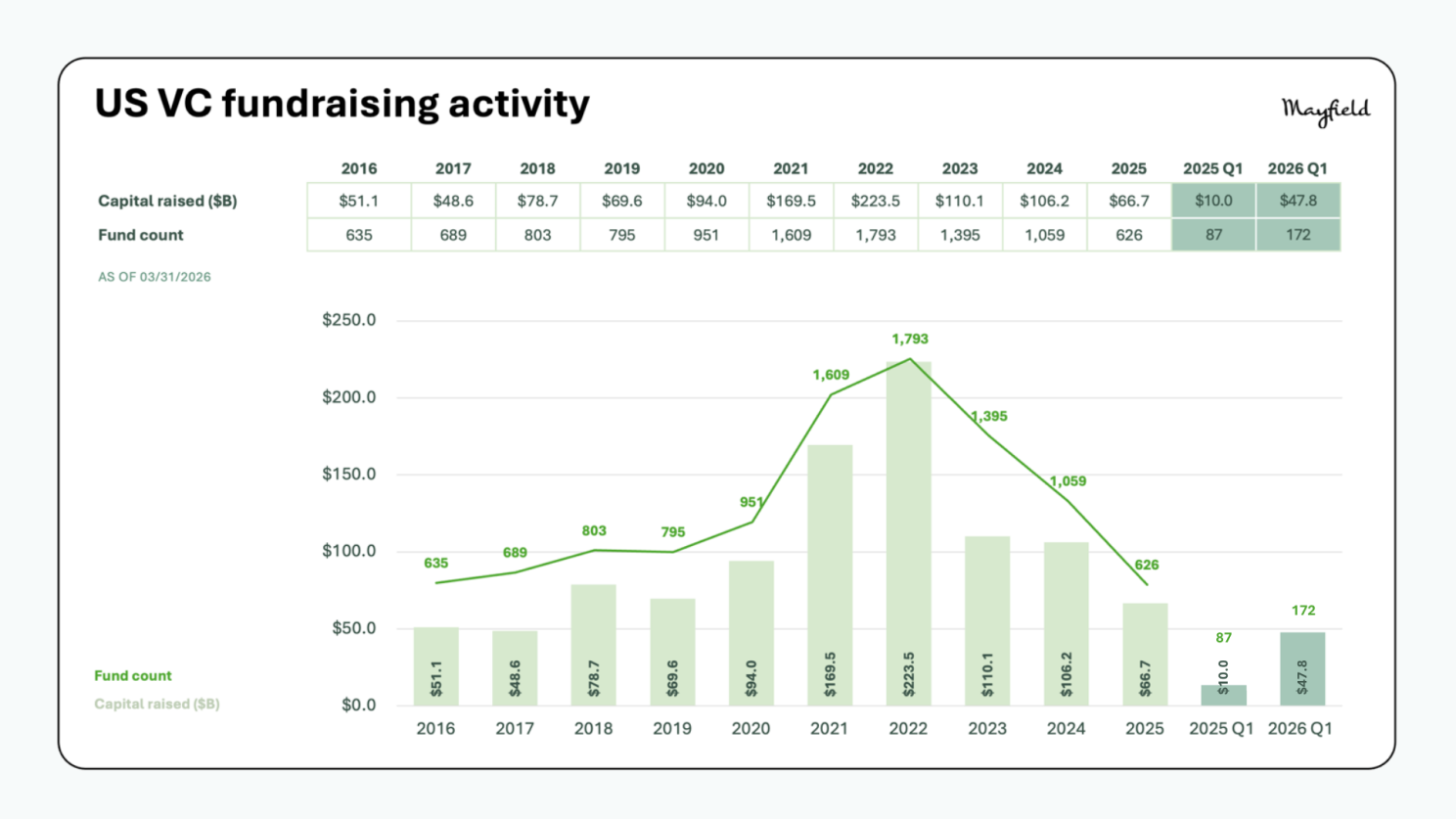

Venture capitalists raised $47.8 billion across 172 funds in Q1 2026 alone. To put that in perspective, the full year of 2025 saw $66.7 billion raised. If this pace holds, 2026 will be among the largest fundraising years this decade.

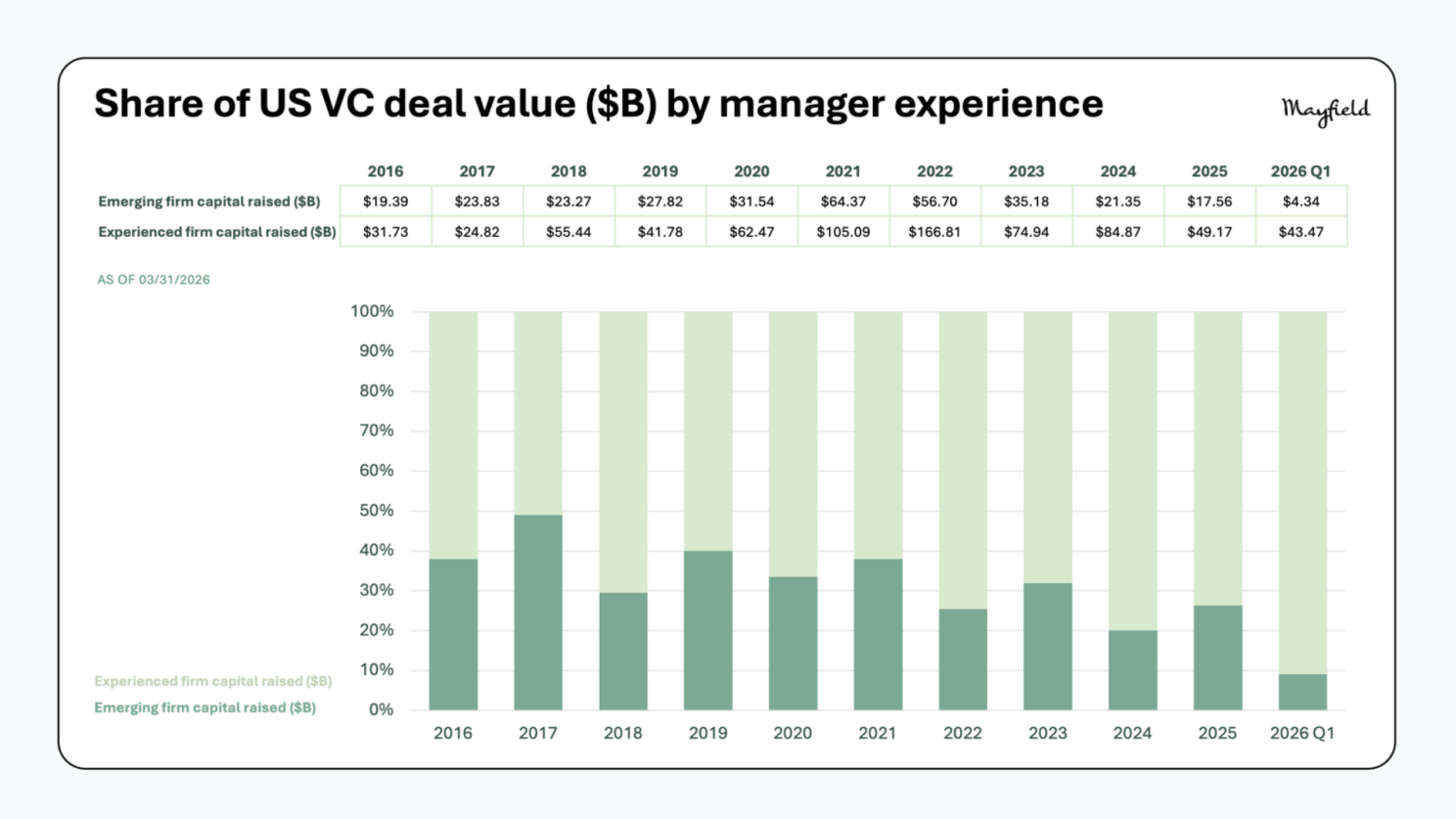

Six “mega-funds” raised 76% of all capital committed in the quarter. Experienced managers, those who’ve raised four or more funds, captured 90.9% of all capital raised, the highest share on record. First-time and emerging managers are effectively frozen out: emerging firms raised just $4.34 billion in Q1, compared to $43.47 billion for established ones.

In my 2026 Venture Outlook, I described a market where 50% of all 2025 capital went to just 0.05% of deals, roughly seven or eight deals. I called it a “narrow slice.” The Q1 2026 data shows the narrow slice has become a needle-point:

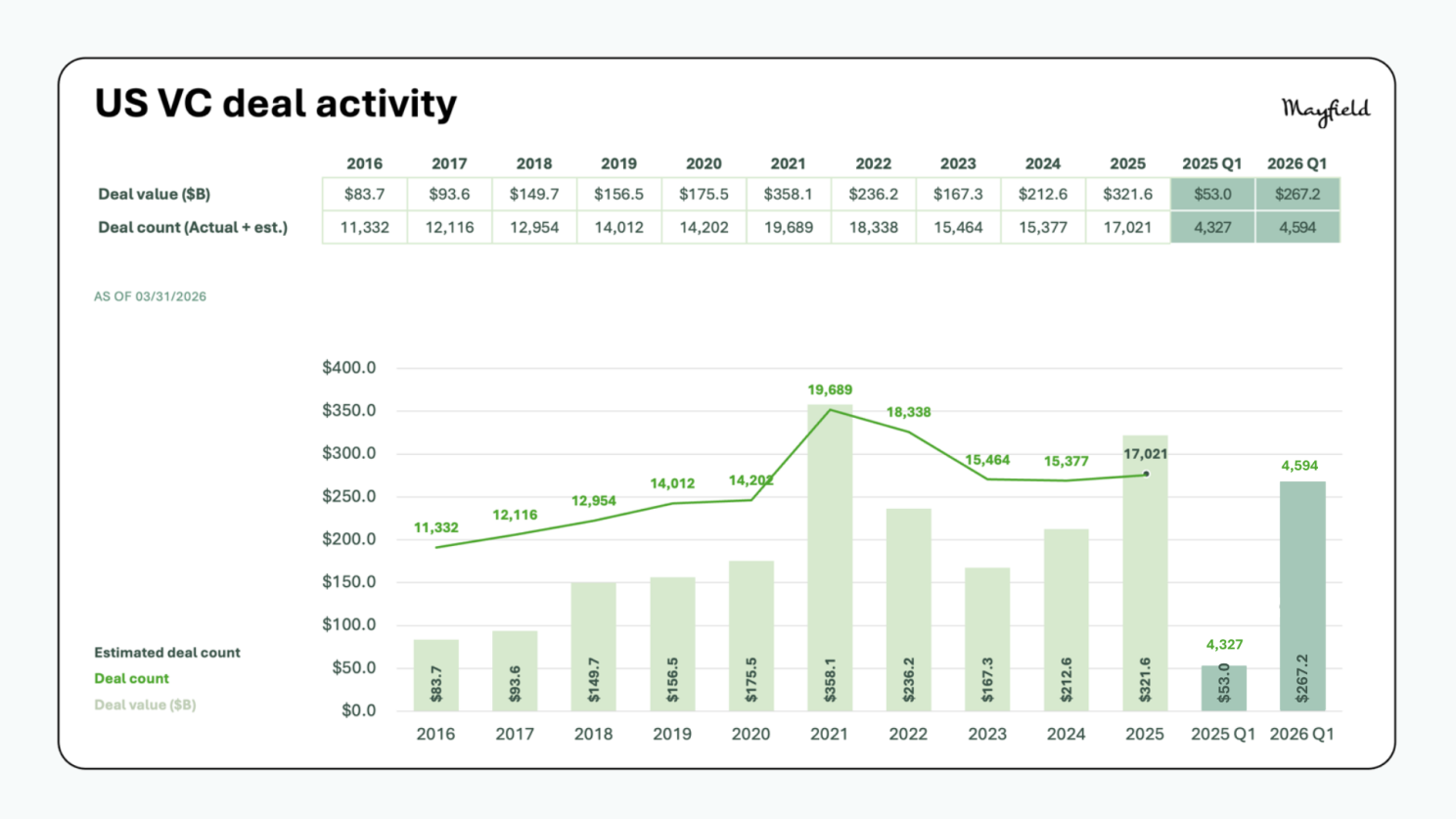

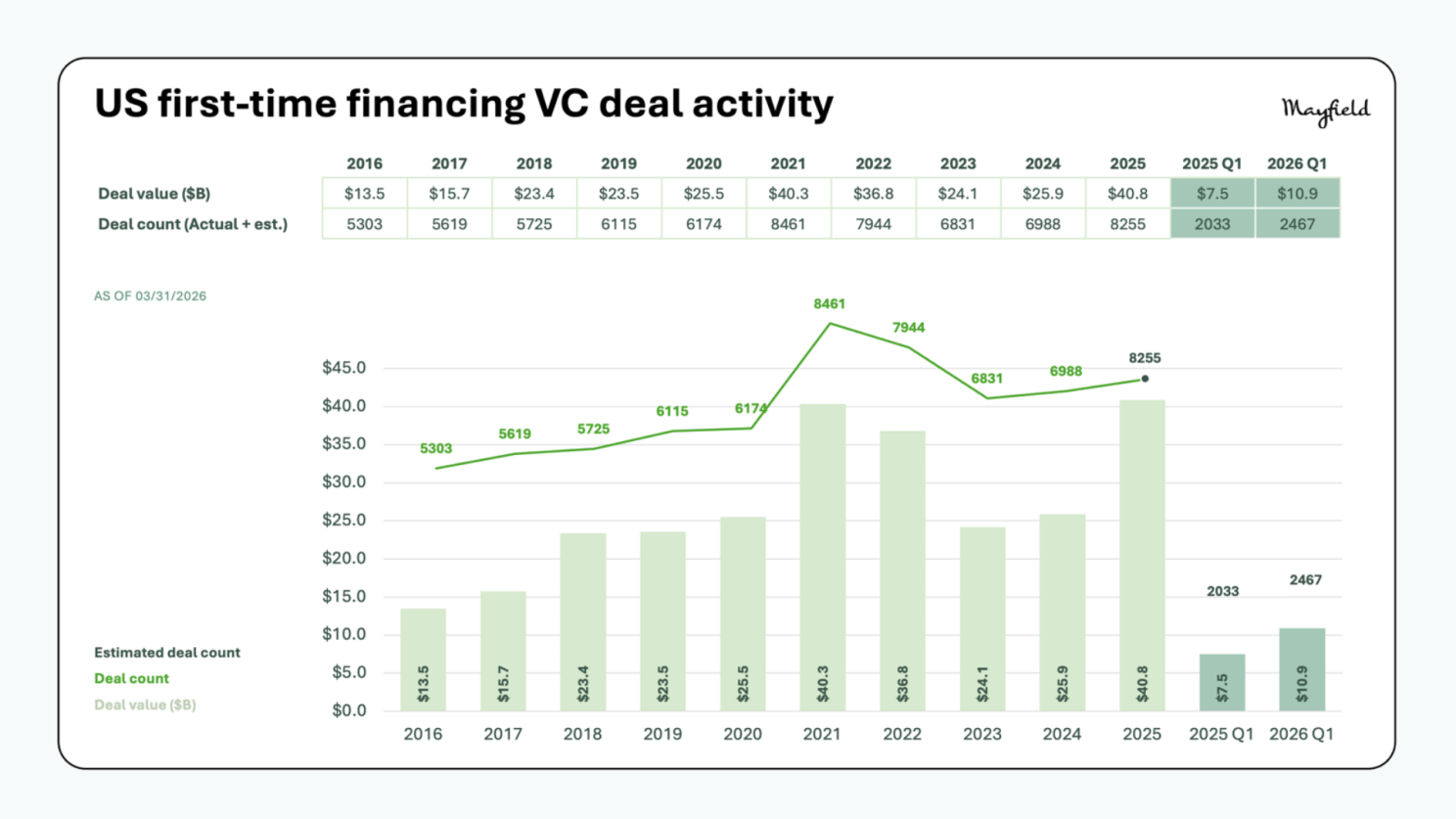

Beneath those numbers, early-stage remains a bright spot. First financings and Seed/Series A rounds are holding strong, as new companies are being formed and funded at scale — an estimated 2,467 first financings in Q1 alone, on pace to surpass 2025 levels.

Bottom line: Early-stage is healthy, but the market is compressing faster at the top. More companies are being created, but capital is concentrating more aggressively into a handful of perceived category leaders. Founders must position their companies as category-defining leaders from day one. The question investors are asking is, “Why will you be the winner?”

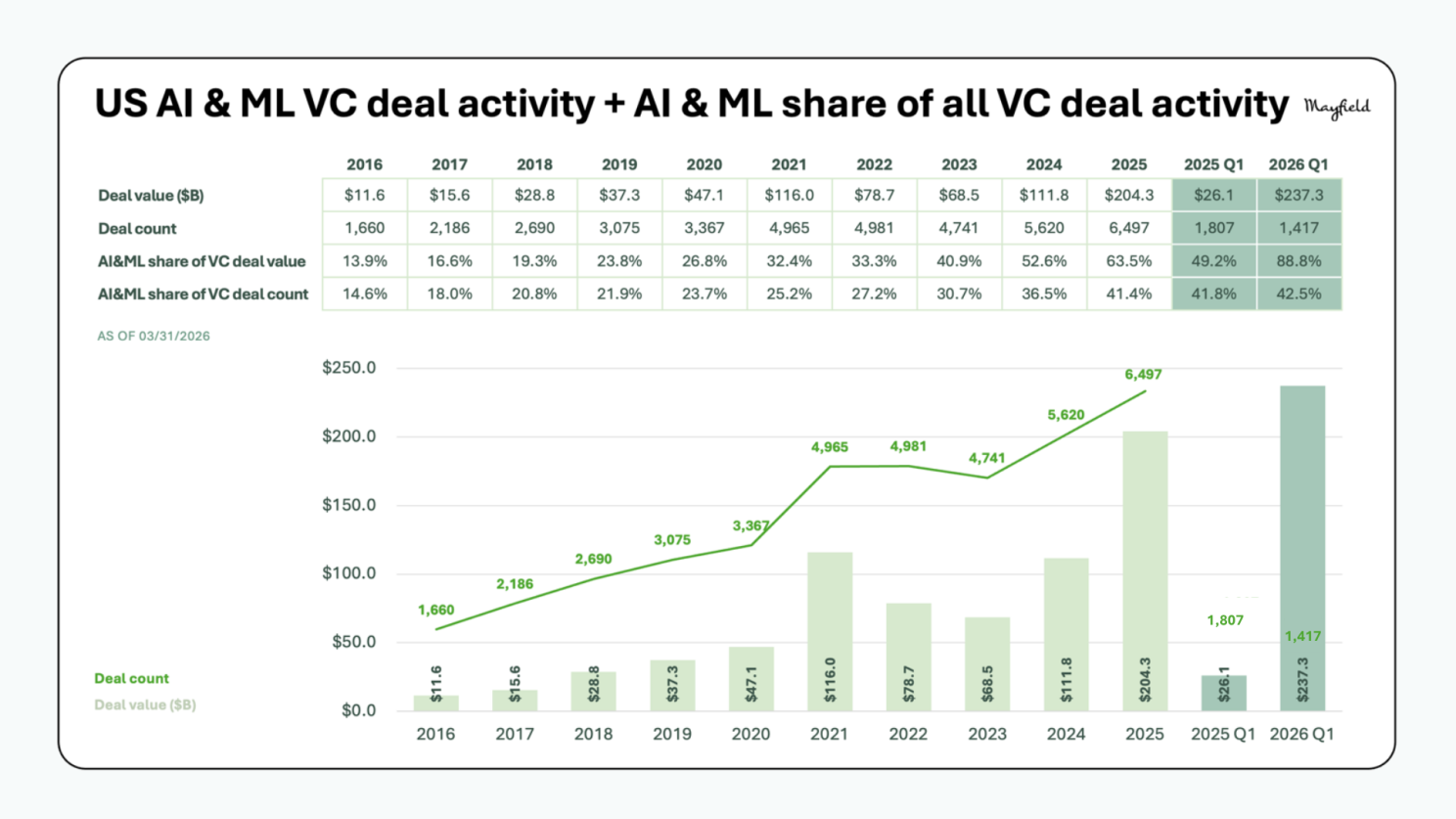

By the end of 2025, AI represented ~65% of all VC deal value. AI now commands 89% of all US venture deal value.

In Q1 2026, AI deal value reached $237.3 billion, surpassing the entire full-year 2025 AI total of $204.3 billion.

Bottom line: Capital is flowing only to AI companies. Everything else is competing for the leftovers.

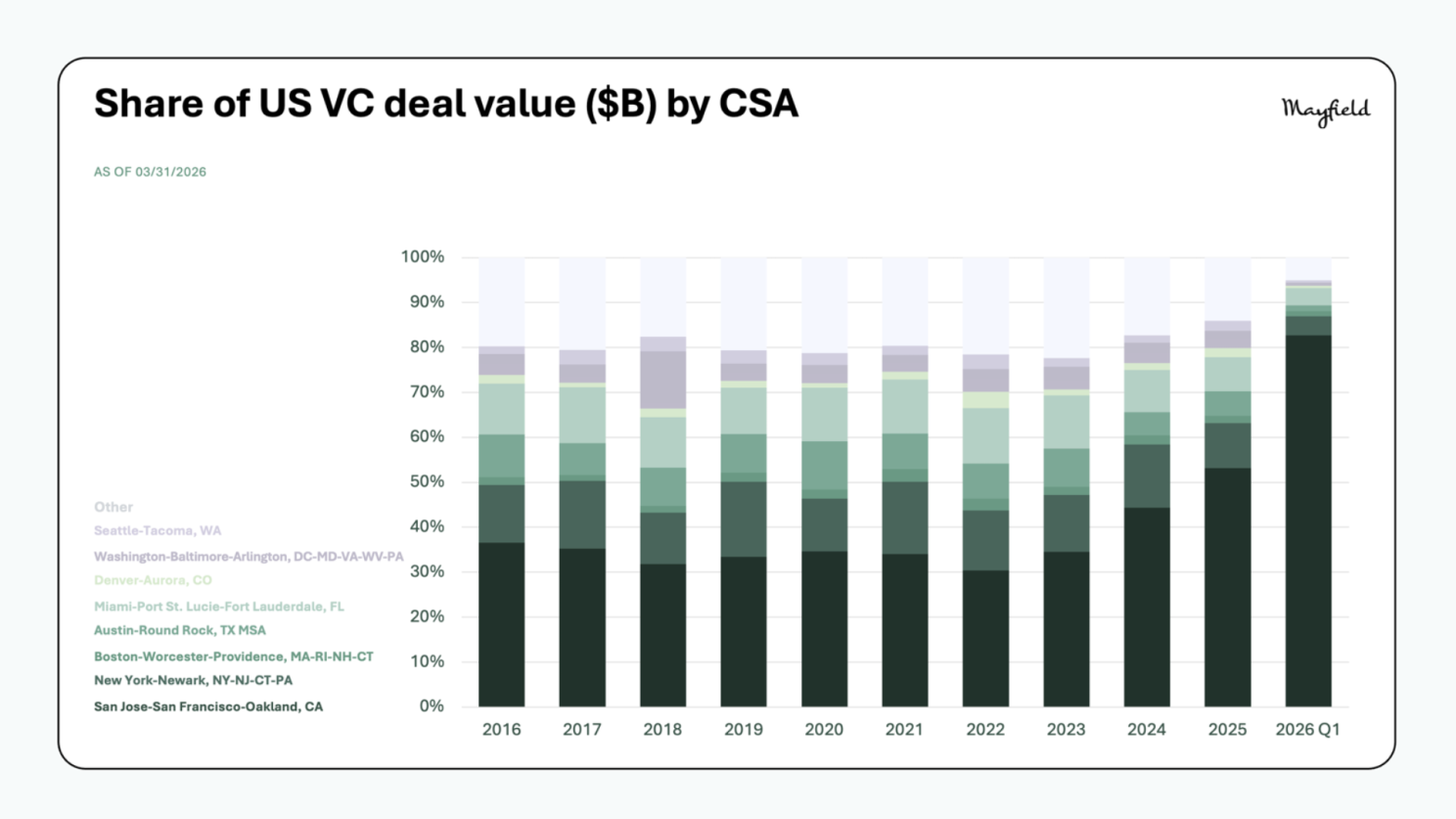

In my 2026 Venture Outlook, I wrote that “AI is the gravitational force pulling capital back to tech ecosystems.” The SF Bay Area alone captured 52.4% of all US VC deal value in 2025.

In Q1 2026, 90.9% of VC dollars went to a handful of major hubs. The SF Bay Area alone captured $221 billion — 83% of the entire $267 billion deployed in the quarter. Virtually every other geography has been compressed into the remaining 16.3%.

The density of frontier AI talent, compute infrastructure, research institutions, and foundational model companies in the SF Bay Area has created a concentration dynamic. Capital follows opportunity, and right now, that opportunity is overwhelmingly localized.

Bottom line: Geography is a gatekeeper to an AI company’s competitive advantage. Everything is happening in the SF Bay Area – and for founders competing at the highest level, physical proximity to dense AI ecosystems is a structural requirement.

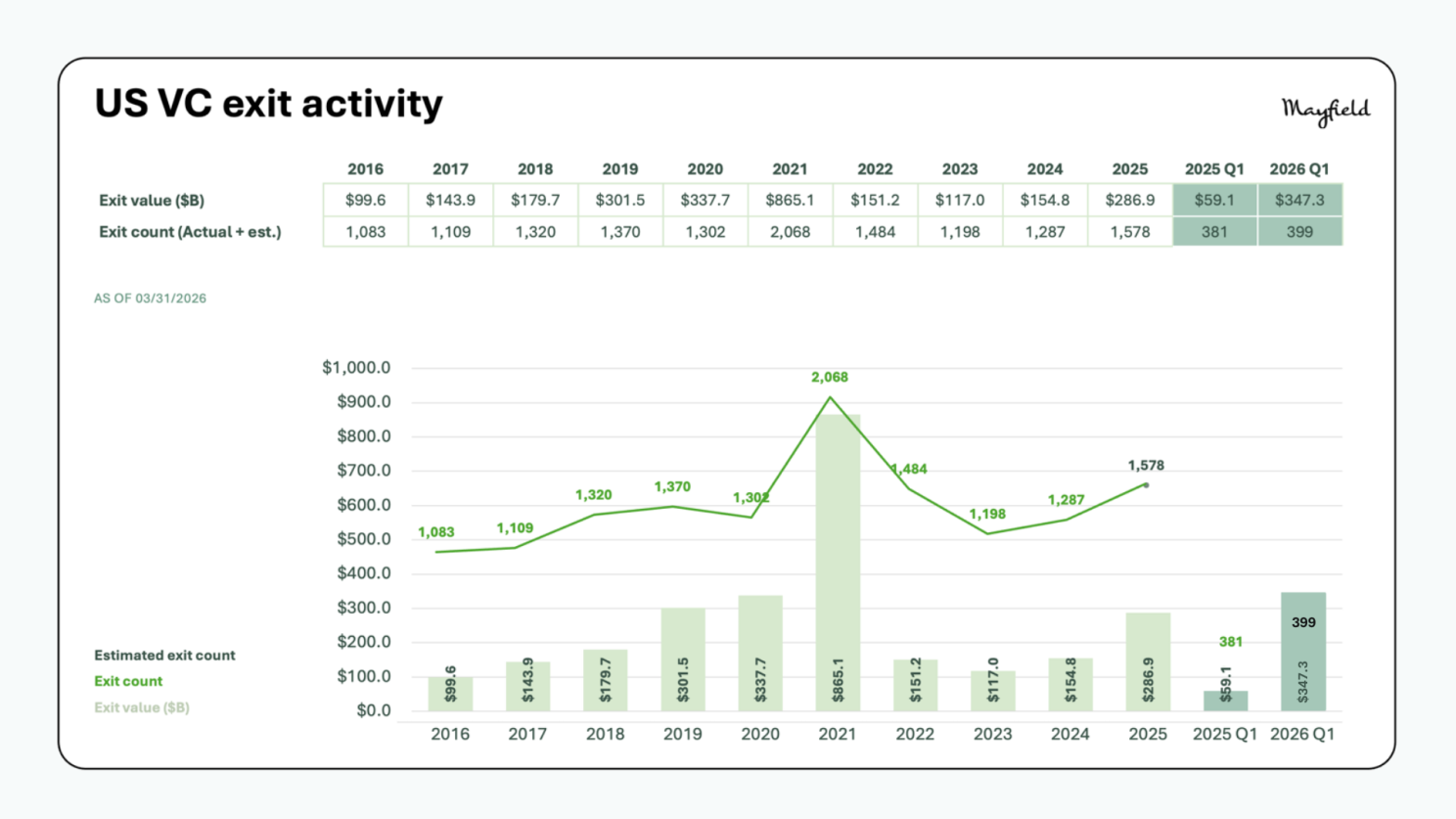

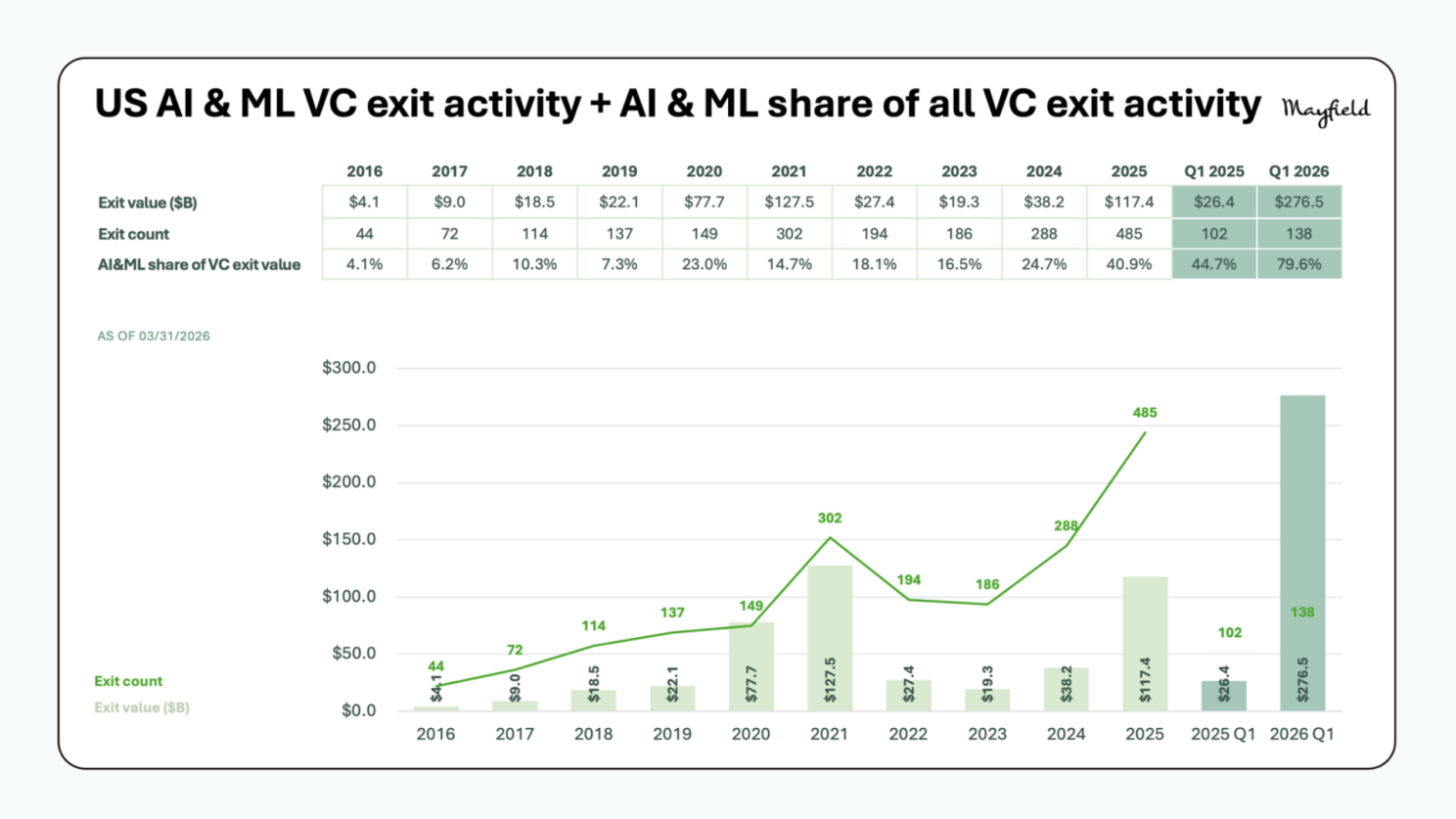

Total exit activity for the quarter reached a record $347.3 billion. AI accounted for nearly 80% of that ($276.5 billion), nearly doubling AI’s 41% share of exit value from full-year 2025. The quarter was headlined by xAI’s historic $250 billion exit in February, the largest VC-backed private exit of a US company ever.

The exit market has “unfrozen” in terms of value, but the thaw is extraordinarily selective. Liquidity is real, and it is flowing almost entirely to AI category leaders.

The traditional IPO window remains challenged. Market volatility, geopolitical uncertainty, and the looming shadow of potential mega-IPOs from SpaceX, Anthropic, OpenAI, Databricks, and Stripe are influencing investor behavior. Venture secondaries have stepped in, reaching ~$95 billion in 2025, and continue to grow as a structural liquidity channel alongside IPOs and M&A.

Bottom line: Liquidity has returned, but only for mega-scale companies. The path to exits is open, but narrow. Build for scale, durability, and leadership.

The most important pattern across all of this Q1 2026 data is bifurcation. Median versus average deal sizes are diverging. Early-stage activity is strong, but driven by dry powder and speed. Meanwhile, more than $5.8 trillion in unicorn value remains locked with limited near-term liquidity.

What looks like a universally healthy venture market at the top masks real structural pressure for founders outside the power law.

Bottom line: This is a two-speed venture market. The winners are scaling faster than ever. The rest face longer timelines, tighter capital, and uncertain exits.

The Q1 2026 data reinforces and intensifies every trend below:

The Golden Era for startups is real. In Q1 2026, we are now in the AI Power Law era. The companies, funds, and geographies inside the power law are experiencing historic abundance. Those outside it are navigating a fundamentally different market.

In my three decades in venture capital and building startups, I have never seen a single quarter like Q1 2026. The next generation of iconic companies will be shaped by the forces this data reveals.