In my two prior editions of Founder Insights, Why 2025 is the Start of a Golden Era for Startups and The Golden Era for Startups: 1H 2025 Venture Outlook, I made the case that we were entering the best era for company building in a generation. The full-year 2025 data from NVCA-PitchBook Venture Monitor is now in, and the thesis holds. $339.4B in invested capital in startups. The amount of capital raised by VCs dramatically dropped to $66.1B. AI captured a record 65% of all VC dollars. Early-stage investing nearly regained the intensity of 2021.

But with one big caveat: this golden era is not evenly distributed. Capital is concentrating in fewer deals, fewer firms, and fewer geographies than at any point in the past decade. Here are five takeaways from the data, with actionable advice for founders navigating this market.

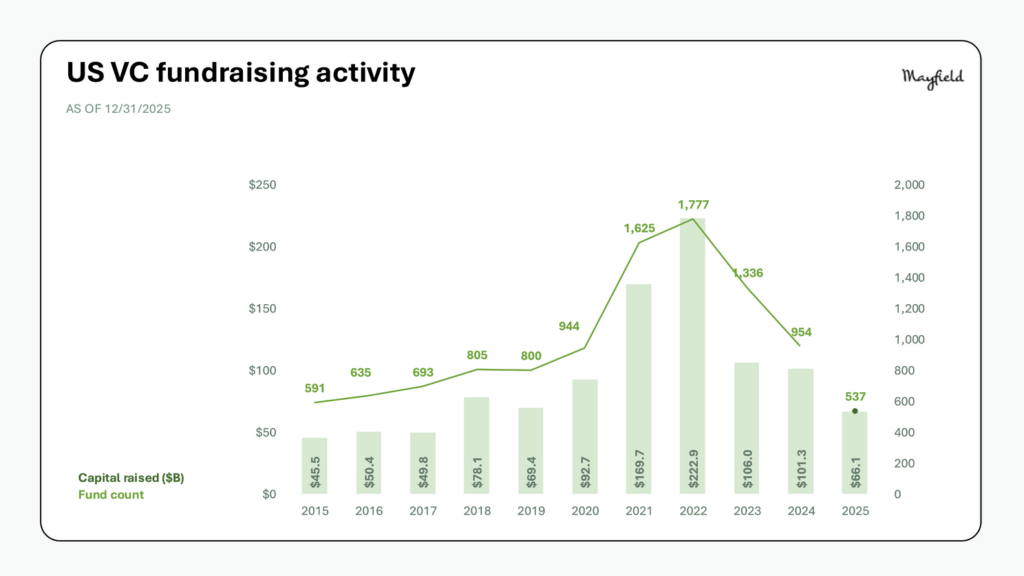

The VC fundraising market hit its lowest point in a decade. Only $66.1B was raised across 537 funds.

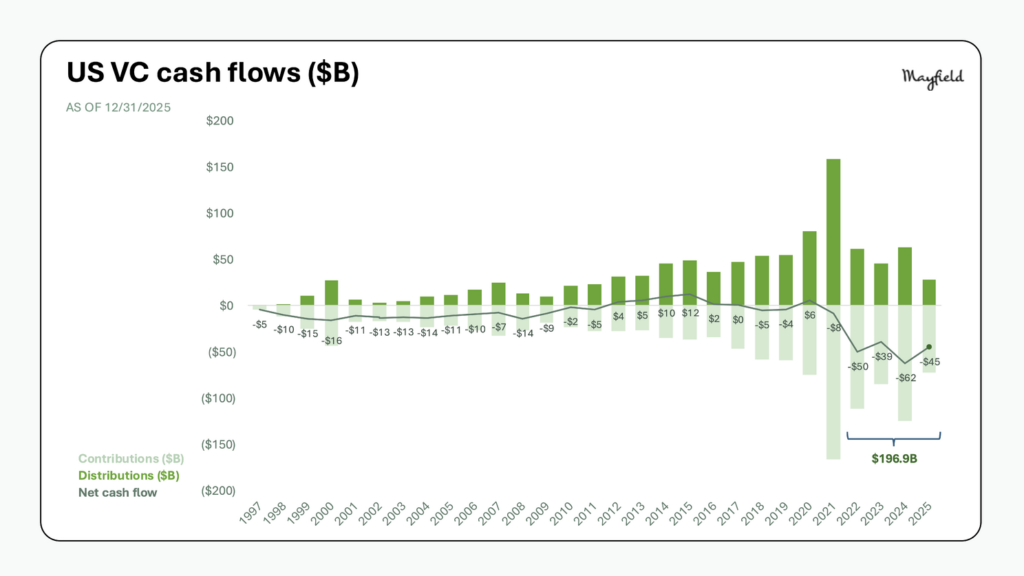

The cause is straightforward: LPs are cash-starved. Net cash flows to LPs have been negative ~$200B since 2022, limiting their ability to recycle gains into new vintages.

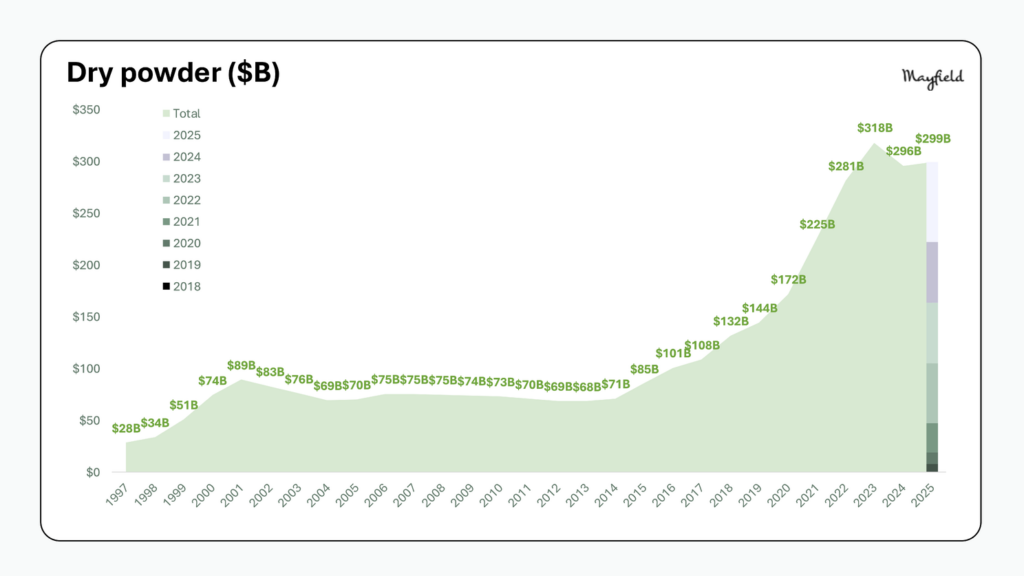

The capital that remains is concentrating fast. Nearly $300B in dry powder sits undeployed, but over 50% is controlled by funds of $500M or more. These large, established firms are dominating deal activity, especially at early and seed stages. First-time and emerging managers had one of their worst fundraising years on record.

Bottom line: Relationship-building with a small set of established firms matters more than broad outreach. Warm intros and alignment with their filters are crucial.

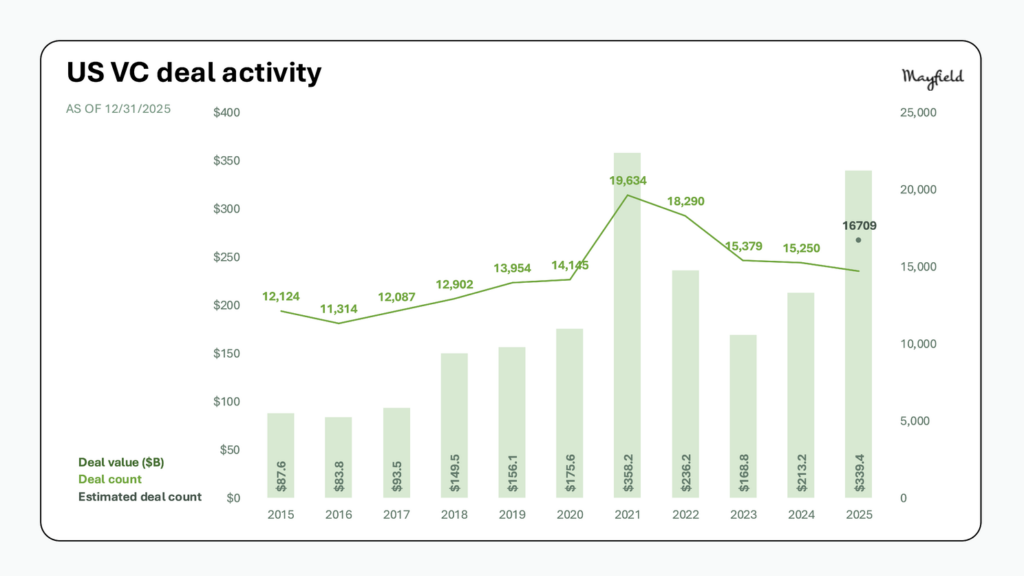

Despite the liquidity headwinds, 2025 deal value reached $339.4B, just 6% below the 2021 peak. That number sounds healthy, but 50% of total deal value went to just 0.05% of deals. The market is active, but capital is flowing into a remarkably narrow slice.

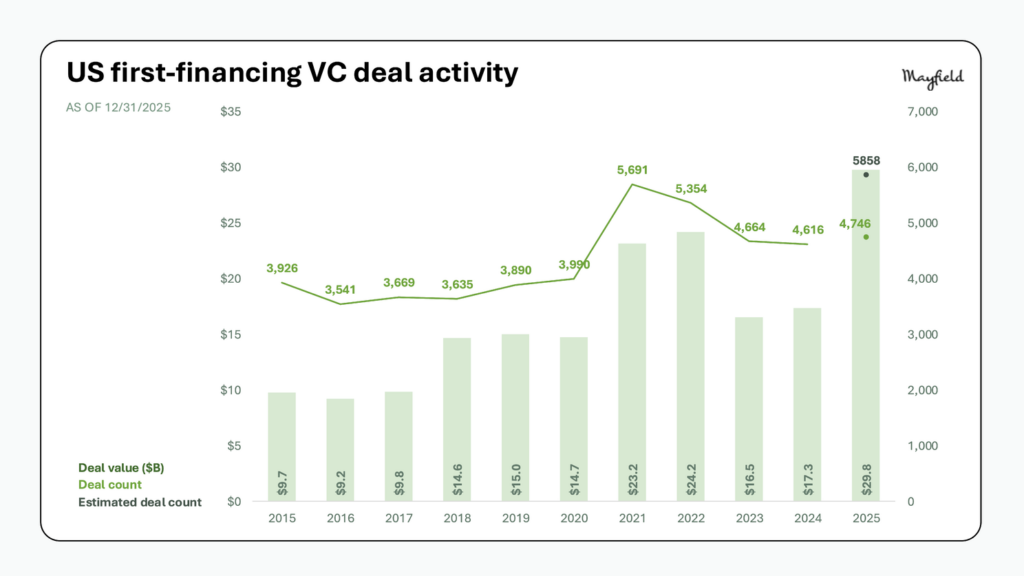

The bright spot is early-stage. First financings and early-stage rounds nearly regained the intensity of 2021, with deal counts and values climbing across pre-seed, seed, and Series A rounds. Investors are actively backing new companies, but they’re concentrating their bets on potential category winners.

Bottom line: You must clearly articulate why you will be a category winner. If you’re not building toward clear category leadership, fundraising becomes significantly harder as capital concentrates around a small set of potential winners.

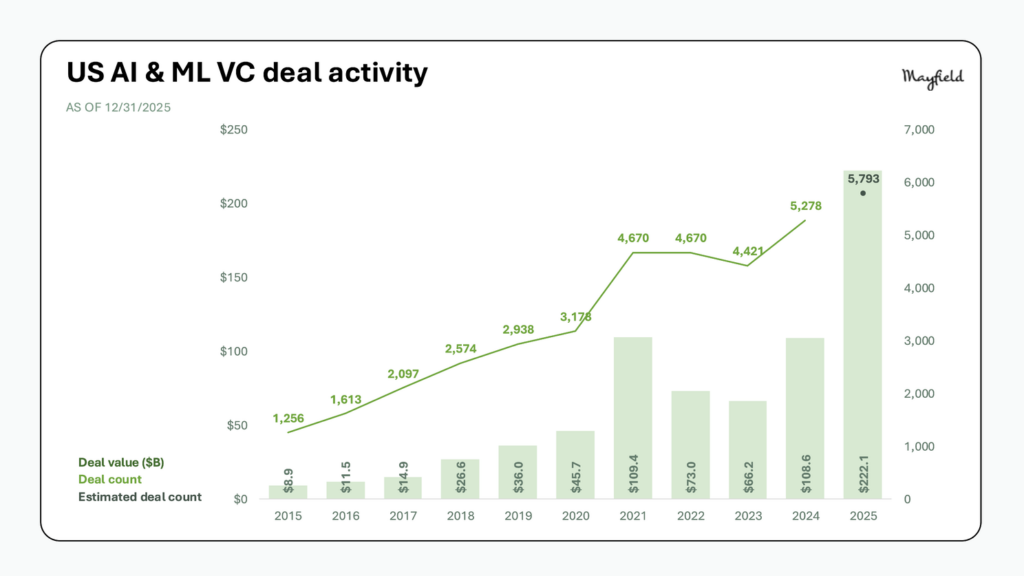

This is the most important structural shift in venture capital. AI and ML accounted for 65% of all 2025 deal value and close to 40% of deal count. A record 5,793 AI deals closed. Average AI pre-money valuations reached $1.19B, up from $358M just one year earlier. That’s a 3.3x jump in a single year.

The VC market’s recovery is fundamentally AI-led. Capital is flowing into foundation models, infrastructure, and AI-native applications across every vertical.

Bottom line: Treat AI as a must-have like water and oxygen, not positioning. AI should be embedded in your product, workflows, and unit economics, so it compounds over time.

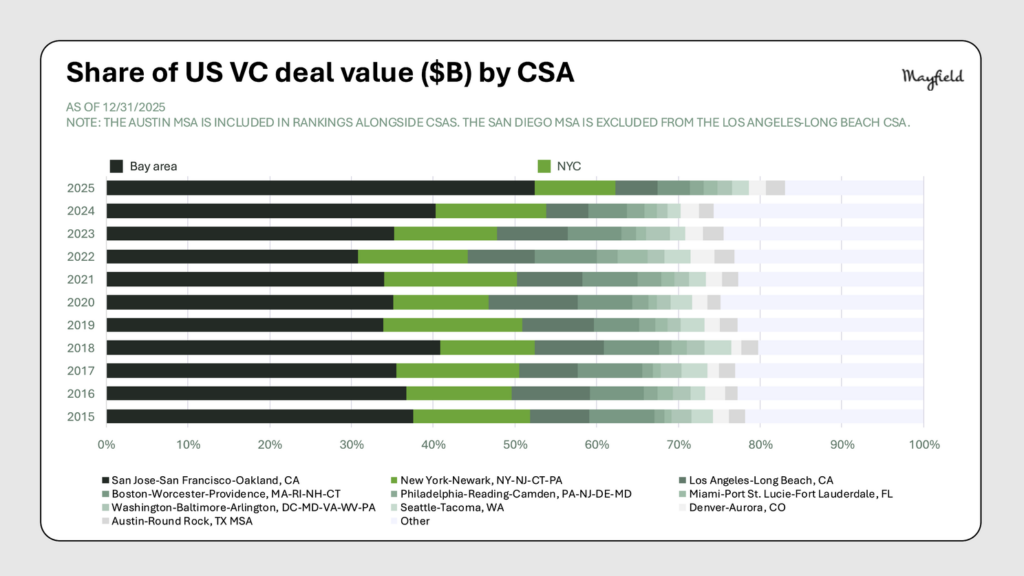

The pandemic-era narrative of geographic dispersion is dead. The Bay Area and NYC now capture 64.2% of all U.S. VC deal value. The SF Bay Area alone captured 52.4% – more than half of every venture dollar invested in the country. AI is the gravitational force pulling capital back to tech ecosystems.

Bottom line: Be intentional about where you build. Physical proximity to dense AI ecosystems accelerates access to talent, partners, and high-quality capital. Geography is back as a competitive advantage.

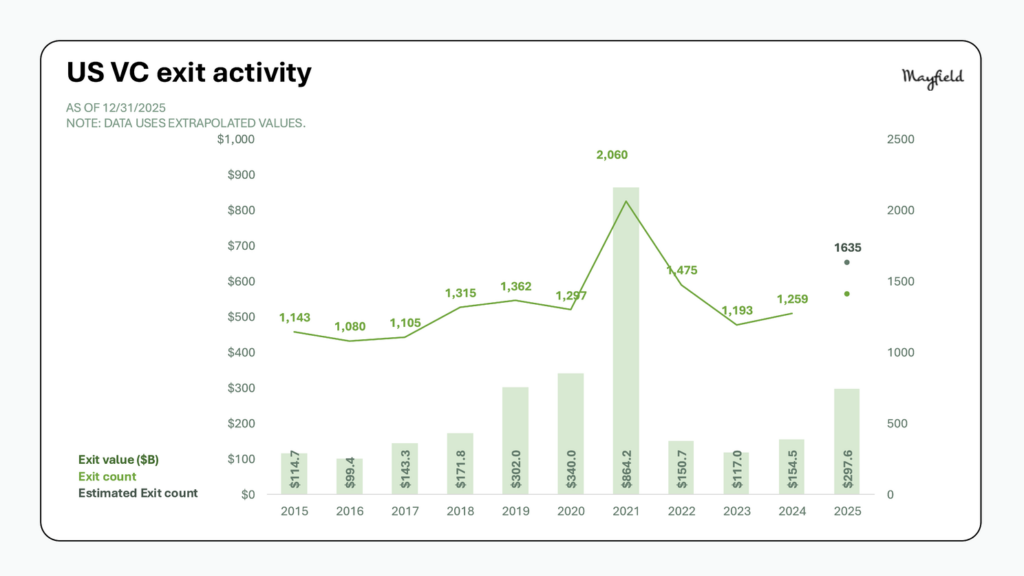

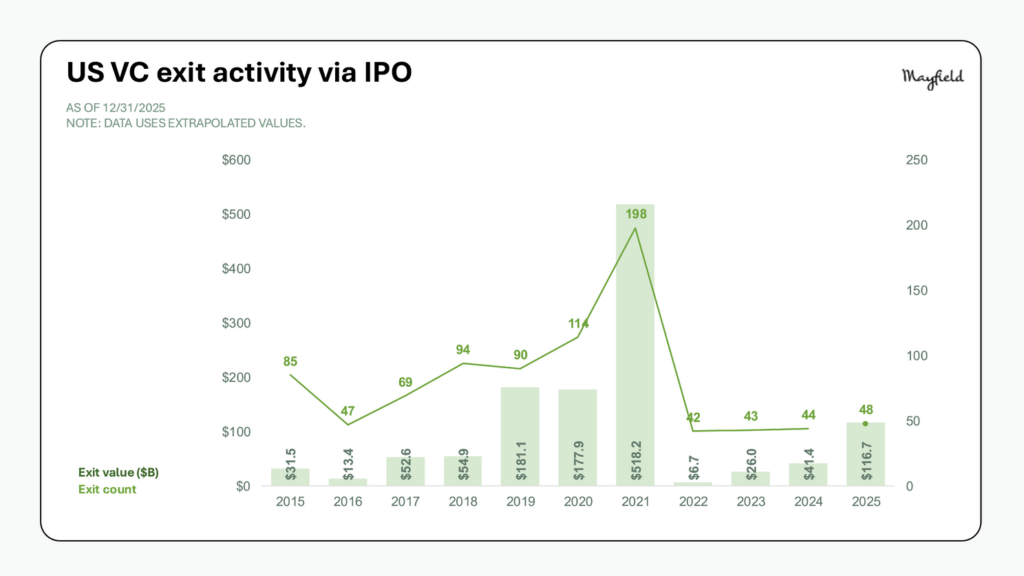

2025 produced $297.6B in exit value, the fourth-best year of the past decade.

Seventeen unicorns went public with much fanfare, but the full picture is more complex. Total IPO count remained muted at 48 listings. A shifting policy landscape constrained exit momentum in 2025.

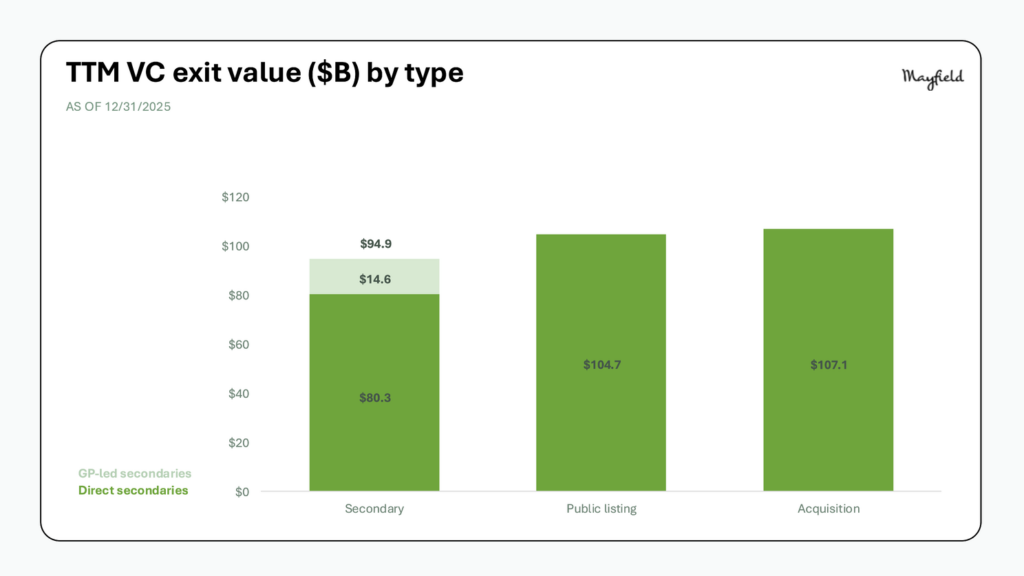

Venture secondaries reached ~$95B, establishing themselves as a structural liquidity channel alongside traditional IPOs and M&A.

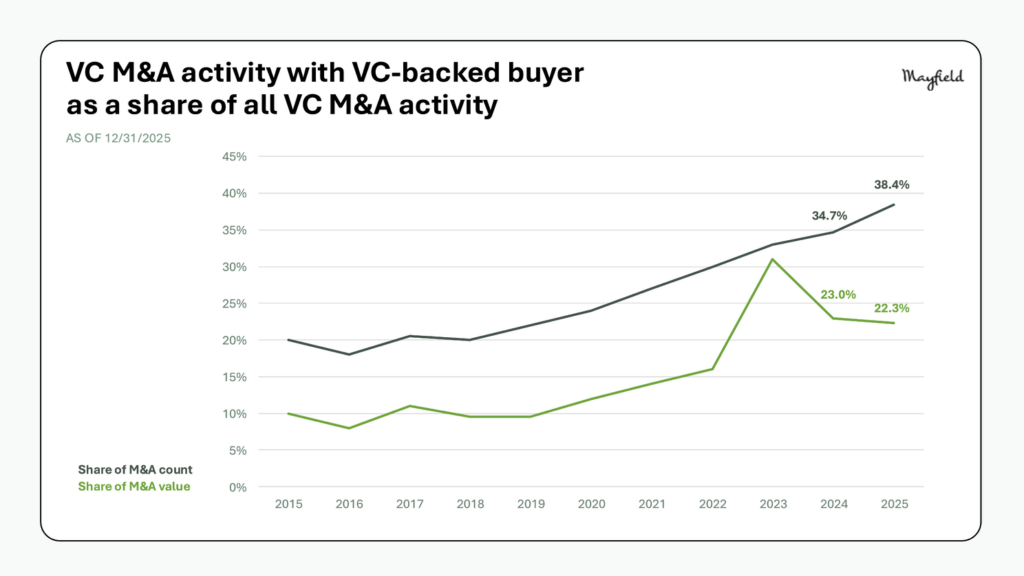

The most significant shift: 38.4% of M&A activity was driven by VC-backed startups, not Big Tech. Founders now have more exit paths, but they need to plan for longer private timelines.

Bottom line: Building a sustainable business matters more than chasing headline valuations. Plan for longer private timelines and multiple outcome paths. An IPO is only one path, and in today’s public markets, not the only plan. Remember, company-building is a marathon, and only the category winners will be worth owning at the end.

Capital is concentrating in fewer deals, fewer firms, and fewer geographies than at any point in the past decade. Where you build now determines who funds you, who joins you, who you partner with, and how fast you compound advantage.

In summary, here are the five takeaways for navigating this winner-takes-most era:

Looking ahead: three shifts will matter more than all the noise combined.

These are just three of the trends shaping the next phase of AI-driven company building. Read the full list of my 2026 AI predictions here.