The LLM era automated cognition. The next era of Physical AI automates labor.

For the past three years, AI has been an information revolution. Better chatbots. Smarter copilots. New productivity tools. Now agents. That is digital AI. It automates cognition.

Physical AI, or what I am calling Labor as a Service (LaaS), is different. What’s coming is $30T in labor-market targeting – every manual, repetitive, and hazardous task in the real economy – across manufacturing, agriculture, logistics, and infrastructure.

Perception, Reasoning, Action: The Physical AI Stack

Physical AI =Foundation models + real-world sensors + actuation + control systems.

It combines three capabilities:

Perception. Vision, touch, audio, and multimodal sensing. The ability to understand a 3D environment in real time, not from a dataset, but from the world as it is right now.

Reasoning and planning. World models, simulation, reinforcement learning, and foundation models working together to make decisions in dynamic, unstructured settings.

Motor control. Robotics, drones, autonomous vehicles, and industrial automation. The ability to translate a decision into physical action with precision, speed, and safety.

This is AI moving from “bits” to “atoms.” And that changes everything about how value is created, captured, and defended.

The “Why Now” Convergence of Physical AI

Three enabling forces are converging at once.

Embodied foundation models. LLMs have graduated to VLAs (Vision-Language-Action). We finally have models that translate 3D scenes directly into motor commands. This is AI moving from language to physics.

The sim-to-real leap. High-fidelity simulators like NVIDIA Isaac and Omniverse allow robots to “experience” 10,000 years of work in a weekend. Synthetic data, computer-generated “memories” of edge cases too dangerous to test in reality, is collapsing training costs.

Hardware inflection. We are seeing massive hardware cost compression, making mass deployment viable. Compute is shifting from GPU-heavy rigs to custom edge AI chips. Sensors like LiDAR are moving from expensive mechanical units to cheap solid-state components.

Individually, none of these forces is new. Together, they unlock the Physical Labor as a Service category.

Key Bottlenecks for Physical AI

Physical AI is harder than digital AI. Not because the technology is early. Because the problem is fundamentally harder.

Data is expensive. You can’t scrape the internet for robot arm movements. Embodied data is hard to collect, context-specific, and costly to generate at scale. This is why simulation matters so much, and why companies with deployed fleets have a compounding advantage.

Long-tail risk is real. In software, a bug can create a poor user experience. In the physical world, errors break things or hurt people. The cost of failure is categorically higher, which is why safety certification and reliability track records become moats, not features.

Hardware iteration cycles are slow. Software updates overnight. Hardware doesn’t. Design cycles, manufacturing constraints, supply chain dependencies, and physical testing all add time. Founders who underestimate this burn capital waiting.

Unit economics are unforgiving. A robot must compete with $15 to $30/hour labor and flexible human adaptability. If your system can’t deliver lower fully-loaded costs that factor in maintenance, power, and hardware cycles, you have a science project, not a business.

Strategic Physical AI Themes to Watch

Four themes will shape which companies define this category.

Robot foundation models. Pretrained, transferable control models that work across different robot platforms. If achieved, this is a major unlock. It would compress development cycles, reduce data requirements, and accelerate category growth. But the timeline is uncertain. Unlike language, physical control requires physics-grounded world modeling and cross-robot training that don’t yet exist at scale.

Simulation-first companies. Training in simulation, fine-tuning in the real world. This approach is compute-heavy but scalable. The sim-to-real gap is shrinking, and companies that master this loop will have a structural advantage in training costs. The biggest breakthroughs in Physical AI may ultimately come from advances in simulation, not hardware.

Vertical-first approach. Winning companies will likely start in one use case, with tight feedback loops and strong hardware-software integration. General-purpose robots may emerge later, but the near-term winners go deep, not wide. Depth beats breadth when the platform layer is still forming.

Enabling infrastructure. This is often underappreciated. Robot operating systems, fleet management, safety layers, edge AI chips, low-cost perception stacks, and data pipelines for embodied learning. The picks-and-shovels layer of Physical AI. Every deployed robot needs this stack, and the companies that own it will collect tolls for years.

Market Landscape: Where the Value Shows Up First

Not all Physical AI markets mature at the same speed. The opportunity unfolds in three layers, each with different risk profiles, capital requirements, and timelines.

Industrial automation is the near-term winner. Warehousing, manufacturing, agriculture, construction robotics, and logistics. These win first because the environments are structured, the ROI is clear (labor shortage, safety, productivity), and deployment cycles are faster. This is not a forecast. It is already happening.

Humanoid and general robotics is the mid-term bet. Warehouse workers, factory assistants, elder care, and hospitality. The vision is compelling, but the challenges are real: dexterity, reliability, safety certification, and cost curves all remain hard. Humanoids are more capital-intensive and have longer horizons than industrial automation.

Autonomous systems are strategically important but highly regulated. Autonomous vehicles, drones, defense, and maritime autonomy. These categories are governed by regulation as much as technology. The timelines are long, the stakes are high, and the winners will likely be companies that navigate policy as skillfully as they navigate engineering.

Bottom line: Start where the ROI is clearest, and the environment is most structured. Industrial automation is the entry point. Everything else builds from there.

For founders, the strongest starting points share four characteristics: highly repetitive workflows, structured environments, high labor churn, and measurable ROI within 12 to 24 months. That means warehousing, food processing, construction sub-tasks, agriculture harvesting, and infrastructure inspection. These are not glamorous. They are high-value. Narrow scope means fewer edge cases, faster deployment, and cleaner data loops.

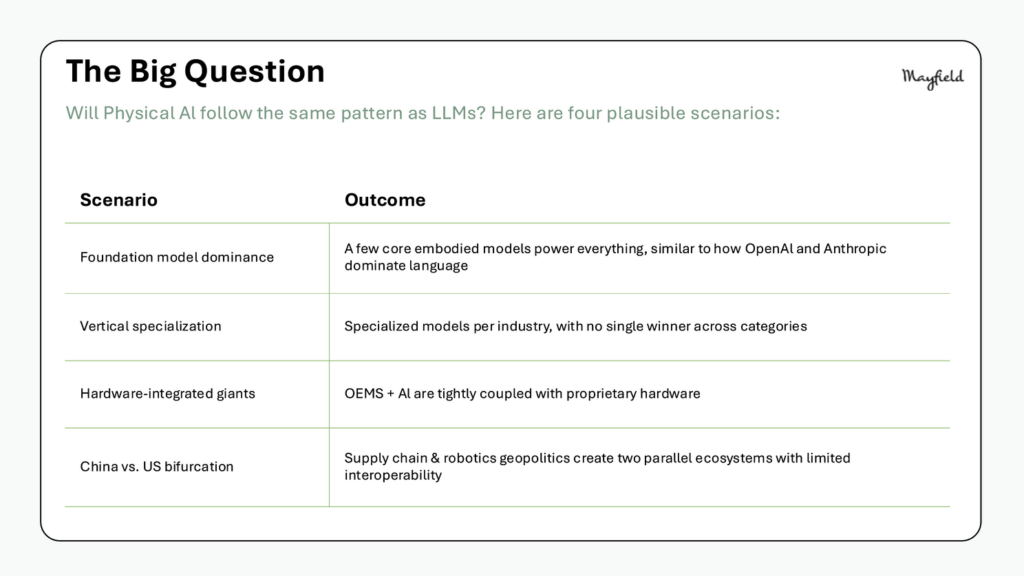

Physical AI: One Platform or a Thousand Verticals?

The likely outcome is a hybrid of vertical specialization and foundational layers. Foundation models will handle basic motion and control. Deep vertical specialization will handle industry-specific reliability, safety, and workflow integration. The companies that combine both will be the most durable.

This matters for founders because it shapes where to build. If you believe in foundation-model dominance, you build applications on top of it. If you believe in vertical specialization, you go deep and own the full stack in one industry. If you believe in the hybrid, you start vertical and build toward a platform over time.

The Strategy Playbook for Physical AI Founders

Physical AI is hard. Everything in this piece has made that clear. But the structural tailwinds are real, and they are not going away:

Global labor shortages are accelerating

Aging populations in developed economies are compounding the problem

Onshoring and reshoring are increasing the demand for domestic automation

Industrial demand operates on long cycles

This combination of forces means Physical AI can produce multi-decade industrial leaders who are building durable infrastructure for generations to come.

If you’re building in Physical AI, here’s what I’m sharing with founders:

Solve the “Pain Test.” Target dull, dirty, or dangerous tasks where labor shortages are structural. Specificity reduces edge cases, safety risk, and data requirements. Start painfully narrow. The narrower your wedge, the faster you learn and the cleaner your data loops.

Design your learning loop on Day 1. Every deployed unit should make the next one smarter. If you don’t have an automated data pipeline from the field back to the model from the start, you’ll have to retrofit it later at enormous cost.

Wedge over a platform. Start with one high-value, repetitive workflow. Generality comes from deployment density, not lab scaling.

Obsess over deployment, not demos. Build operational excellence early. The companies that win this category will be the ones that master the unglamorous work of field ops, maintenance protocols, and customer integration.

Sell work, not SaaS. Physical AI is not sold like a software subscription. Use Labor as a Service (LaaS) to turn a risky CapEx buy into a predictable labor expense.

Hire operators, not just researchers. Winning teams combine ML researchers, control engineers, embedded systems talent, manufacturing expertise, and field-deployment ops.

Raise capital aligned with hardware timelines. Hardware iteration cycles are slow. Supply chains are complex. You need longer runways and patient investors who understand that Physical AI compounds gradually, not exponentially.

Scale only after reliability is proven. Scaling before you’ve hardened your system is the fastest way to burn capital and credibility.

The winners won’t be the most viral. They will be the most operationally disciplined.

Labor as a Service is Coming

Physical AI is real, capital-intensive, and slower than the LLM hype cycle. It is also more durable and potentially more economically impactful because it targets the $30T+ global labor market, not just information work.

It will reward patience, deep technical diligence, hardware literacy, and long-term capital. This is not 12-month MVP territory.

The next iconic AI companies won’t just be smarter tools. They will redefine how physical work gets done as Labor as a Service.

Bottom line: Digital AI moats are built in the cloud. Physical AI moats are built on factory floors. They take longer to build. But once built, they are far harder to displace.